The Correct Prophecy

Keynes predicted our AI future precisely. He just got the beneficiaries completely wrong.

The year is 1930. The world is in free fall. The stock market has shed nearly half its value since the crash. In the United States, thousands of banks have failed or suspended operations. Bread lines stretch around city blocks in New York. Unemployment across Europe is rising fast. And John Maynard Keynes, the most celebrated economist of his generation, sits down at his desk in his rooms at King’s College, Cambridge, and writes an essay about leisure.

Keynes was 47. He had lived in those Cambridge rooms since he was an undergraduate. His wife Lydia was upstairs. Lydia Lopokova had arrived in England with the Ballets Russes, dancing under Diaghilev, and had somehow stayed, first as a sensation and then as Keynes’s partner, to the bewilderment of his Bloomsbury friends who thought the match beneath him. She read the draft of his new essay and reportedly told him it seemed too optimistic. She was right, but not in the way she meant.

The essay was “Economic Possibilities for Our Grandchildren.” Keynes was explicit, almost aggressively so, that he was not describing the present. He was forecasting 100 years ahead. The Depression was, in his view, a temporary turbulence on top of a much longer and more powerful trend. Compound interest works. Technology compounds productivity. Over a century, these two forces operating together would solve what Keynes called the “economic problem,” the age-old human struggle to meet basic material needs. By somewhere around 2030, he predicted, the standard of living would be between four and eight times what it was in 1930. The working week would shrink to fifteen hours. The central challenge of that future would not be production. It would be something harder: “how to occupy the leisure which science and compound interest will have won for him, to live wisely and agreeably and well.”

I have been reading that essay with something close to dread, because it is so right about the technology that the reading gets uncomfortable.

The Three Predictions and What Happened to Them

Let me give you the 2026 version of Keynes’s forecast, data point by data point.

On productivity: PwC’s April 2026 global AI performance study confirmed that AI is generating extraordinary economic gains at scale. The top-performing firms in the survey are seeing productivity and revenue impacts that, by historical standards, are remarkable. We are in the middle of what may be the largest single productivity event in the history of industrial capitalism.

On leisure: Stanford University published a controlled study this month showing that AI assistance produces efficiency gains of between 76 and 176 percent on standard digital tasks. Workers with AI tools finished their work significantly faster. They then used the freed time predominantly for leisure. Netflix. Earlier departures. Keynes worried specifically that people might “misuse” their leisure, fill it with accumulation rather than enjoyment. The Stanford subjects opted for something closer to enjoyment. The leisure arrived, more or less as described.

On the end of the economic problem: Goldman Sachs estimates that AI is currently eliminating around 16,000 net US jobs per month. Those 16,000 people per month are experiencing the leisure economy Keynes envisioned. They did not choose it, and they cannot afford it, but they have it.

The prophecy arrived. I just want to be precise about where it landed.

PwC found that 75 percent of AI’s economic gains are being captured by the top 20 percent of firms. The remaining 80 percent of companies are seeing minimal gains, or net losses after implementation costs. The Keynesian windfall is being collected by a fraction of the economy, while everyone else gets either the bill or the involuntary leisure.

Lydia was right. The essay was too optimistic. Not about the technology. About who would receive it.

Evan Spiegel’s 11 Percent Morning

On April 15, Evan Spiegel, the CEO of Snap, announced that the company would lay off 1,000 employees, roughly 16 percent of its workforce. The company also disclosed that 65 percent of its code is now generated by AI. The stock jumped 11 percent before the markets opened.

Spiegel is a useful character for understanding the 2026 moment. He co-founded Snapchat at Stanford at 21, turned down a $3 billion acquisition offer from Mark Zuckerberg while he was still young enough to be carded at bars, and became one of the youngest self-made billionaires in history. He is not reckless or ideological. The Snap layoff is, by any conventional financial logic, the correct decision. AI writes 65 percent of the code. You pay fewer engineers. The savings produce $500 million in annual cost reductions. Investors reward the discipline. The stock goes up 11 percent. Every number in that chain of reasoning is accurate.

What makes the announcement worth pausing on is not any individual decision but the arithmetic it represents. Sixty-five percent of output is automated. Sixteen percent of the workforce is released. Shareholders capture the productivity gain. The engineers who remain are now responsible for a codebase they did not write and cannot fully audit. As I argued when writing about the Validator Class last January, this is deskilling wearing the costume of efficiency. The engineers kept their jobs. Their job description did not.

The workers who lost their positions are now experiencing Keynes’s leisure economy. The shareholders who captured the productivity gain are experiencing Keynes’s wealth economy. The distance between those two groups, measured in that 11 percent pre-market jump, is the entire argument.

The technology is working exactly as Keynes said it would. The distribution is working exactly as Keynes assumed it would not have to.

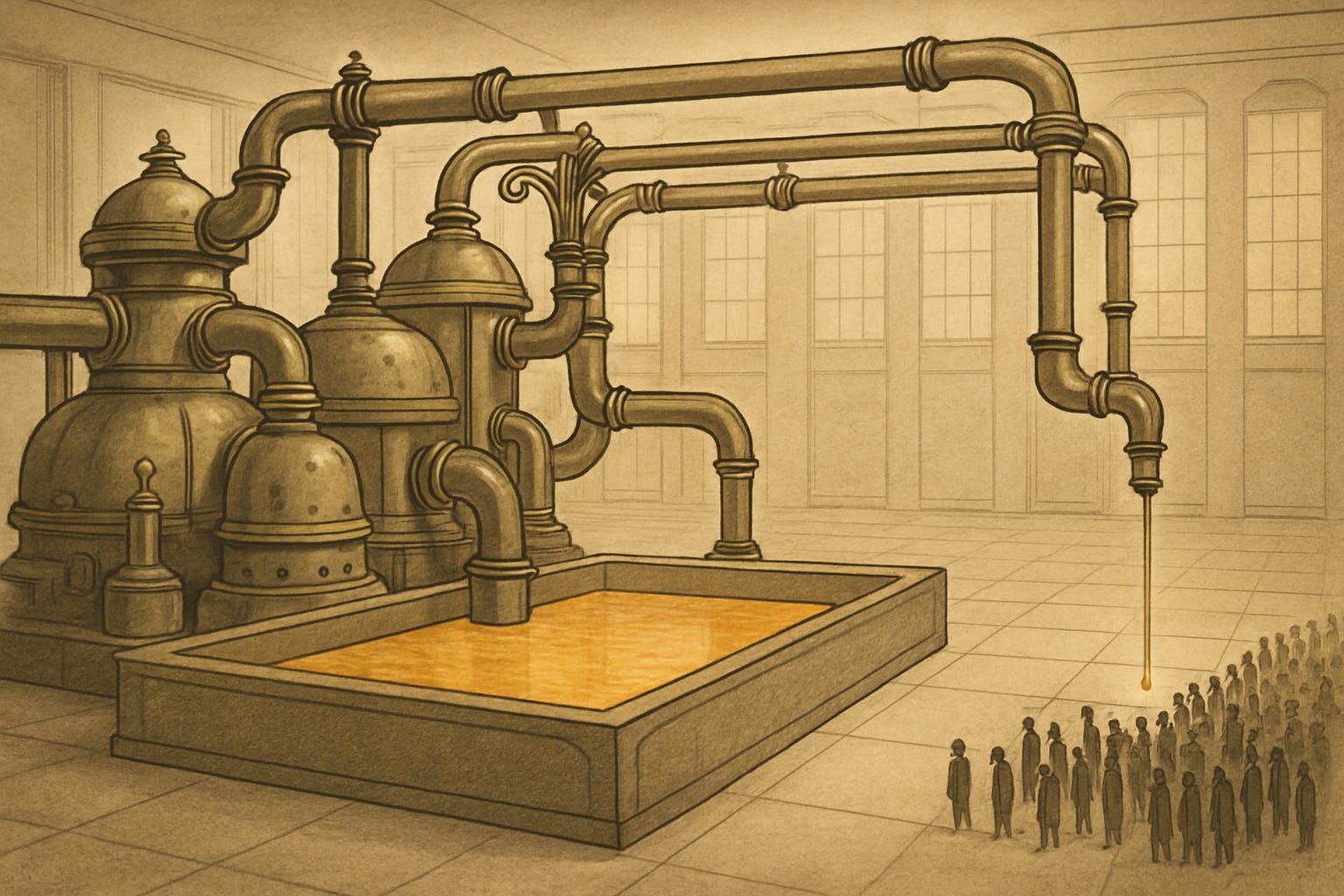

The Economist Who Thinks About Pipes

Anton Korinek is not famous in the way that economists who appear on television are famous. He works carefully, publishes precisely, and says things that are true rather than things that are reassuring, which tends to limit one’s media profile considerably. Born in Vienna, trained at Columbia under Joseph Stiglitz, now a professor at the University of Virginia’s Darden School and a senior fellow at the Brookings Institution, Korinek has spent the better part of a decade building formal economic models of what happens to labor markets when AI becomes genuinely transformative. His papers have titles like “Preparing for the (non-existent?) future of work” and “Aligned with whom?” and they have a quality that is unusual in academic economics: they answer the question they pose.

His central finding, stated plainly, is this. The distributional outcome of AI is not determined by the technology. It is determined entirely by institutional choices. If capital owns the AI and labor does not, the gains flow to capital. If policy redistributes those gains through wages, taxation, or mandatory profit-sharing, they flow broadly. The technology itself has no preference. The pipe is not neutral. The pipe is a political object, and it can be designed in more than one way.

I find Korinek’s framing clarifying in the way that useful economic thinking should be: it names the actual variable. The question “will AI make us all richer” is not a technological question. It is a constitutional one. The answer depends not on what the models can do but on who owns them, who benefits when they produce, and what institutional mechanisms exist to distribute the output. Keynes could imagine a world in which the answers to those questions favored broad distribution. He was writing in the shadow of a labor movement that had forced capital to share manufacturing productivity with the workers who produced it. He had reason to think the institutions would follow. He was wrong about what the institutions would do. He was right to think they were the variable.

The Thirty Years That Prove It Is Possible

Between roughly 1947 and 1973, something happened in the United States economy that has not happened since. Productivity and median wages tracked each other almost perfectly. Real wages for the median American worker rose substantially in real terms. The gains from technological progress were shared broadly enough that the living standards of factory workers, office workers, and professionals all rose together. Economists Claudia Goldin and Robert Margo named this the “Great Compression” in their 1992 paper, because what compressed was the income distribution: the gap between the highest and lowest earners narrowed significantly during these decades.

In France, the same period has a different name. Jean Fourastié called it the Trente Glorieuses, the thirty glorious years: a period of roughly 5 percent annual GDP growth that reached deep into working-class life, funding the expansion of French public education, healthcare, and infrastructure in ways that improved how ordinary people actually lived.

Both periods were powered by technology and capital. What made them different from what preceded and followed them was the institutional architecture around that capital: strong unions with real bargaining power, top marginal tax rates in the United States that exceeded 90 percent during the Eisenhower administration, regulated capital mobility that kept investment onshore, and public commitment to education and infrastructure as mechanisms of shared productivity.

I want to be clear about what this history proves. The Keynesian distribution is not a fantasy. It is not a utopian projection. It happened. For thirty years, in two of the world’s largest economies, the pipe worked. Technological gains were broadly shared. Then the pipe was taken apart.

The deregulation movement that began in the late 1970s did not change the technology. It changed the institutions. Unions were weakened. Top marginal rates were cut. Capital flows were liberalized. The mechanisms through which productivity had been shared with workers were removed or hollowed out, one by one, across roughly four decades. The technology kept compounding. The distribution stopped following.

What we are watching in 2026 is the end state of that process. The most powerful productivity technology in human history has arrived into an institutional environment optimized, over forty years, to prevent its gains from being widely shared. Keynes wrote his prophecy before that dismantling began. We are reading it after.

The pipe existed. Someone took it apart. This is not an accident, and it is not irreversible.

Three Ways This Ends

I think about the futures here more than I probably should, and I want to be honest with you about how I see them.

The scenario I worry about most is permanent capture. AI-champion firms use their gains to invest further in AI, widening the advantage over subsequent quarters. Political systems, already substantially shaped by concentrated capital, do not respond at the required scale or speed. The 16,000 monthly net eliminations continue and accelerate. Workers aged 22 to 25, already showing a 16 percent employment decline in AI-exposed occupations since 2022, enter a permanently constricted entry-level market. The Keynesian leisure arrives for more and more people, involuntarily, without the income that makes leisure a gift rather than a sentence. The returns to AI ownership compound faster than the general economy, and wealth concentrates accordingly. This is the default if nothing changes, and I believe it is the scenario most consistent with the institutional environment as it currently exists.

The middle scenario is muddling through, which is also the historical pattern. Labor movements slowly negotiate AI protections into contracts, as ProPublica’s journalists are already fighting for and as Snap’s remaining engineers will eventually demand. States pass imperfect laws requiring impact assessments and notification. Companies discover that over-automating has costs that only appear in year five: a study published this week found that firms cutting workers aggressively may be eliminating their own customer base in ways that quarterly earnings cannot capture. This feedback loop eventually creates its own restraint. Redistribution happens unevenly, over a decade or more, with a transition that is brutal but not permanent. This is how previous technology waves resolved, eventually, if not cleanly.

The version I believe is possible, if we are honest about what it requires, is a response at the scale of the problem. The current scattered signals of political mobilization, anti-AI protests in major cities, union campaigns at newspapers that cover AI, proposed bipartisan federal legislation requiring quarterly reporting on AI-driven job changes, are early and disorganized. But the conditions that historically precede institutional change at scale are all present: concentrated gains, visible pain, and a growing gap between what the technology makes possible and who receives it. The New Deal required a political figure with the imagination to design institutions that had not existed before. Bretton Woods required Keynes himself, in 1944, to design mechanisms for international economic cooperation without a template. What the current moment requires is similar: institutional imagination at the same scale as the technological achievement. That is difficult. It is not unprecedented.

My honest read is that we will get some version of the middle scenario, with elements of the third pushing through wherever political will assembles quickly enough. I am a cautious accelerationist. I believe in the technology. I think the productivity gains are real and extraordinary and capable of improving human life at a scale we have not seen since the post-war boom. I also think that “capable of” and “will” are separated by exactly the kind of institutional work that has never happened automatically and has never happened without sustained pressure from below.

What Keynes Would Find Interesting

Keynes died in 1946, two years after Bretton Woods, not long after his institutional ideas had achieved their greatest global influence. He did not live to see whether his 1930 forecast would come true. He spent his last years exhausted from war work, defending Britain’s interests in negotiations with Americans who held all the economic leverage, watching the international architecture he had designed get built in a form less ambitious than he had wanted.

I think he would find 2026 interesting rather than discouraging. The technology did what he said. The productivity is real. The efficiency gains are real. The leisure is real, if involuntary for many of the people experiencing it. What would strike him, I suspect, is not the failure of his forecast but the precision of the one thing he admitted he could not forecast: how institutions would behave.

He wrote in 1930 that the problem of the future was not production. The problem was distribution. He assumed, perhaps too generously, that the institutions forming around him would solve the distribution problem more or less automatically, the way markets had once solved the production problem. He was wrong about that assumption in a way that forty subsequent years have made impossible to ignore.

The correct prophecy is sitting in this week’s data. PwC has measured it. Stanford has measured it. Goldman Sachs has measured it. The technology produced exactly the gains Keynes said it would. They went to exactly the fraction of the economy that the institutional architecture allowed.

The question is whether the political will to rebuild the pipe assembles before the capture becomes permanent enough to make the question academic.

I do not know the answer. I know which outcome I am working toward.